January 17, 2003

We hope you had a good holiday season and wish you a very happy New Year. Unfortunately, in the realm of investing, the past year was not a good one.

By now most of you must be aware that we have just experienced three consecutive years of negative returns in the stock market – an unprecedented event within the last sixty years. It has been hard to watch baby boomers’ nest eggs wane. It has been gut-wrenching to witness employees, at the brink of retirement, have their whole 401(k)s wiped out, as in the case of Enron.

Many today would agree, and to good measure, that we are not the same nation any more. The yardstick for this being the September 11th, 2001 attacks which manifested our vulnerabilities. Shortly after, things would become worse as our own citizens, entrusted with the highest positions in corporate America, robbed us of our confidence in the very financial system this great country was built on. Alas, that was not the end. Eventually we would get to know that some of our most respected analysts, on whose recommendations we placed our faith, had their own corrupt agendas.

The question is what do we do now? Where do we go from here? As we have always reiterated – we are not prognosticators. If there is one thing that we have learned from the past three years, it is to never try to predict the future. As investment advisors, all we can do is ensure that your portfolios are well diversified, broadly allocated and balanced among all sectors and styles and investment vehicles. The rest is purely systematic or non-diversifiable risk. In layman terms, it is the risk that all companies face when the economy is on its belly or when the economy is jolted by external shocks such as the geopolitical uncertainties surrounding us today.

As we step into 2003, there exist many such uncertainties in the form of global terrorism, the potential war with Iraq, the North Korean nuclear crisis and the lingering recession in Japan. In our own country, we face the prospect of a long-term budget deficit, an investment community skeptical of venturing back into the stock market, a weakening currency, low consumer confidence and a rising unemployment rate.

Nevertheless, there are also quite a few bright spots on the horizon. The consumer has been the cornerstone of our economy over the last several years. Even through the trying times of the last three years, consumer spending has been strong and resilient. Thanks to 12 interest rate cuts by Greenspan & Company, the housing market has never been better. Productivity has been simply scintillating and we are finally experiencing growth, albeit small, after three consecutive quarters of negative GDP in 2001.

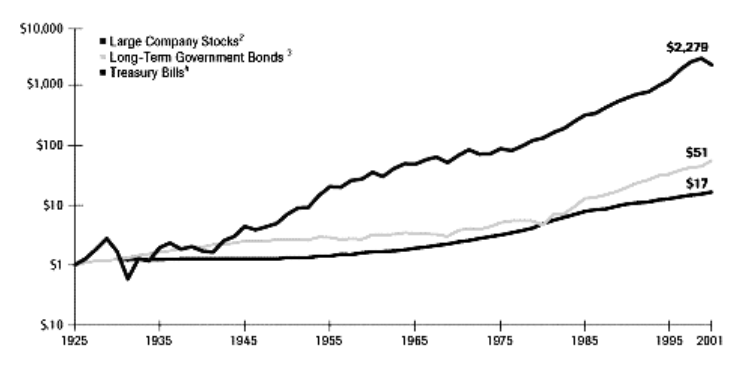

As you can see not all is gloom and doom. As the graph below illustrates, things that go down always do come back. It was so during the dark days of the Great Depression, it was so during World War II, it was also so during the Korean War, the Vietnam War, the oil shocks of the 1970’s, and the high deficit years of the 1980’s. The 21st century should be no different.

Stocks, Bonds and Bills 1925-2001 – Value of a $1 Investment

Source: Ibbotson Presentation Materials, © 2002 Ibbotson Associates, Inc.

Enclosed, you will find your Portfolio Performance Summaries, Portfolio Holdings Statement as of December 31, and a quarterly Account Management Fee Statement. If you desire Morningstar reports or the most recent copy of our Form ADV, Part II, please call us. The year 2002 tax information will arrive by late January or early February.

Sincerely,

President

Portfolio Manager

Investment Assistant